Warren Buffett: In No Rush to Storm His Capital

Looking beyond the headlines actually puts Berkshire’s $300 billion cash pile into better perspective.

Benjamin Franklin once said, “In this world nothing can be said to be certain, except death, taxes and Warren Buffett’s Cash Pile predicting a market crash.”

Alright, maybe one of our founding fathers didn’t say that, but if he were alive today, I'd bet he would. Financial media, permabears and your occasional charlatans salivate when they see Berkshire Hathaway’s cash reserves have reached an all-time high. Why? You ask? Because it is the quickest way to grab your attention. Think about it, the world’s most admired and successful investor has taken profits on some stocks at a time where the stock market is at all-time highs and added to his war chest for the inevitable market crash. I mean he must know something we don’t, right?

You might not like my answer: it’s complicated. Everyone wants the answers, we want to live in a black and white world, we want things to make sense without taking a step back to look at the whole picture. Investing is smack dab in the middle of that black and white world. Whenever you buy a stock, someone just sold it to you. Who is on the right side of that trade? Do they know something I don’t? It’s complicated.

Berkshire Hathaway as of the 3rd Quarter of 2024 has built up a substantial $305 billion in cash and equivalents, mostly in the form of Treasury bills1. $305 billion is a huge jump from just a decade ago where Berkshire only held $57 billion in cash reserves, so the concern is warranted. I believe there are a multitude of reasons for this. Is the sudden increase in cash reflect a bearish call, I don’t believe so. Now, I can’t say I would take the other side of that argument either. Let’s dive in below to see what I mean.

Float On

One must remember Berkshire is made up of numerous businesses. A cluster of those include Insurance companies they have acquired over the years which Buffett states are one of the “Four Giants” driving Berkshire’s value. Berkshire’s insurance companies, which include BH Reinsurance, Gen Re, Geico, just to name a few all possess what the insurance industry call ‘float’. Float are premiums that the insurer has collected and are free to use at its disposal till the claims are paid out. Buffett explains it perfectly here:

“Insurers receive premiums upfront and pay claims later. ... This collect-now, pay-later model leaves us holding large sums -- money we call "float" -- that will eventually go to others. Meanwhile, we get to invest this float for Berkshire's benefit. ...”

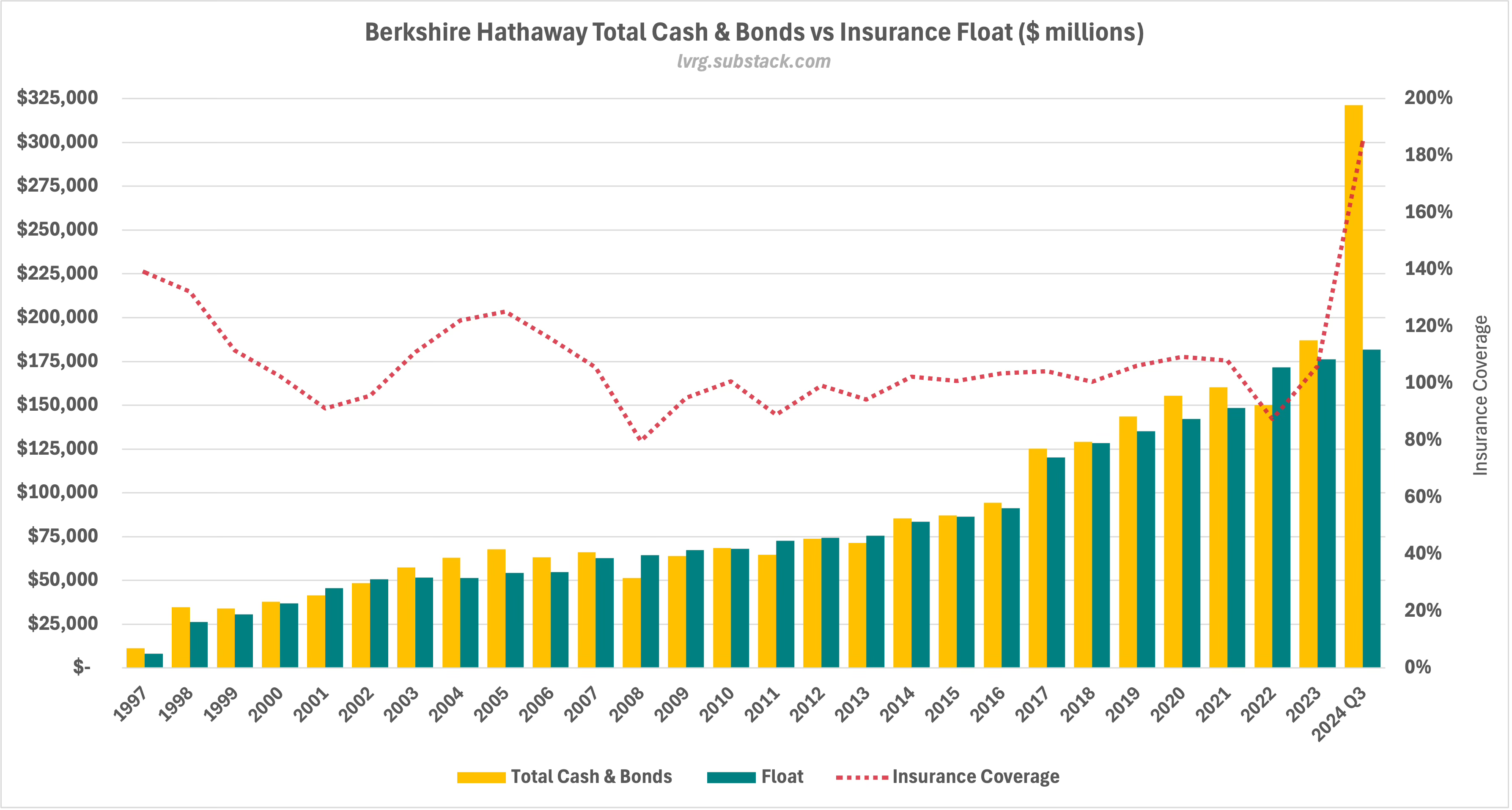

Buffett has maintained his position on keeping capital at a Fort Knox level to preserve Berkshire from any calamities. Over the past few decades, he has done this by keeping Berkshire’s liquid assets (cash, T-Bills and fixed income) roughly in lockstep with the Insurance float.

In the graph above, you can see that for the past 15 years, Berkshire has maintained a close relationship between its liquid assets and insurance float. The red dotted line represents insurance coverage—essentially how much of the float is backed by liquid assets—which has consistently hovered around 100%, indicating Buffett's commitment to keeping these values aligned. However, I'd be remiss if I didn't address the two notable periods when this relationship deviated: the late 1990s and our current moment. However, I’d be remiss if I didn’t address the large swings in insurance coverage pre-GFC. In the late 1990s, Buffett viewed market valuations as extreme and was hesitant to deploy capital. Instead, he built up cash in anticipation of a major acquisition—which materialized in 1998 with Berkshire’s purchase of General Re, adding substantial capital and float. This explains the gradual decline in insurance coverage, as both cash and float expanded at a similar pace.

Not long after, a mix of factors led to Berkshire’s cash reserves surpassing its float. The company’s insurance operations were generating significant underwriting profits and expanding their float, while Federal Reserve Chairman Alan Greenspan was raising interest rates—further swelling Berkshire’s cash pile. At the same time, Buffett recognized the growing irrationality in markets, as Wall Street operated under the illusion that there was no housing bubble. Anticipating trouble, Berkshire continued amassing cash. This strategy proved prescient, allowing Buffett to seize once-in-a-lifetime investment opportunities and position Berkshire as a financial lifeline for struggling companies.

Now, I know what you’re thinking—after reading that, of course, he must be preparing for a market crash. Just look at history. But before jumping to conclusions, let’s take a broader look at what else could be driving this historic cash buildup. After all, history doesn’t repeat itself, but it does rhyme. And this time, the buildup wasn’t gradual—it was a massive jump in a single quarter. That alone is worth a closer look.

In the next part, I’ll dive deeper into the key factors behind the massive jump in cash that Berkshire has amassed – beyond just market timing. There are more structural, strategic and economic reasons at play that would explain why Buffett isn’t in a rush to deploy any capital.

ABCs (Apple, Bank of America and Cash)

A massive jump in cash that Berkshire had from the end of 2023 to this most recent quarter Q3 2024 is a bit peculiar, to go from $163B to $305B is significant. A substantial contribution to the jump in cash came from sales of two of Berkshire’s top holdings, Apple and Bank of America (BofA). At one point the Apple position became worth nearly $175B (effectively 50% of the equity portfolio) until Buffett started to trim the position along with BofA which had amassed into a $41B position itself.

Materially, little has changed with Apple and BofA, sure the valuations are a bit stretched but I can confidently say the “story” or the reason Buffett bought them have not drastically altered.

At the last Annual Shareholder meeting Buffett himself alluded to the elephant in the room anyways when a question was asked about why he sold some of the stake in Apple, his answer, Uncle Sam.

Post-WWII, the corporate tax rate has been in a bear market. In the late 1960’s, it reached its peak at 53% and now find itself 21%. This is not an argument to raise the tax rate, but I think Buffett can see the writing on the wall. It’s political suicide to raise taxes on your constituents and there is no guarantee we can outgrow our debt, so who do you think will fit the bill? You guessed it, Corporate America.

Berkshire’s cost basis for Apple is around $36B and BofA is $14.5B, so you can see that the tax bill would be significant. I think Buffett has figured to rip the band aid off now and potentially avoid a larger tax bill down the road on both investments.

The Final Stretch

With the loss of his right-hand man Charlie Munger just over a year now, I think that has also weighed on him. I think Buffett understands his time at the head of Berkshire is now passed the seventh inning stretch and he is a bit more cautious with capital than he was earlier, which I think is admirable, especially given the sheer size of Berkshire.

I think the timing of all this has worked in Buffett’s favor, we are no longer in a zero percent interest rate environment and with T-bills offering a modest yield above 4%, all that cash is printing money in interest.

“We’d love to spend it, but we won’t spend it unless we think we’re doing something that has very little risk and can make us a lot of money.” Buffett said at that last annual meeting when asked about the growing cash pile. “If we could buy a company for $50 billion or $75 billion, $100 billion, we could do it.” “It would be easier to do with a private company,” he said. “And there aren’t very many that are big. On the other hand, there’s nobody else that can quite make a deal like we can, under the right circumstances.”

Now of course, there are multiple companies in the S&P 500 that Berkshire could acquire but as he said, it’s easier and can be done in a shorter time frame with a private company. Now, I believe that statement has some truth to it, but at the same time I think Buffett has some hesitation. I think he is starting to see the horizon on his time making decisions, and this enormous cash pile is his parting gift to his heir apparent, Greg Abel who will take over as CEO when Buffett punches out for the final time.

Instead of tackling an acquisition that could more or less bring on any unknown burdens or liabilities right before he passes the torch on could let Buffett sleep a little better at night. Presenting Abel with an ample balance sheet would give Berkshire a lot of flexibility that I believe any incoming CEO would appreciate.

Now, all of this could be wrong tomorrow when Berkshire’s annual report and shareholder letter is published tomorrow and he explains everything but who knows? I think there is always more that meets the eye, especially when you are dealing with a company of Berkshire’s size nearly a trillion dollars. We can all assume things but at the end of the day, maybe Warren just wants to ride off into the sunset without a worry in the world and having a good chunk of change would accomplish that.

I appreciate reader feedback, so if you’ve enjoyed today’s piece, feel free to like or comment at the bottom of this page!

You will see a number $325 billion floating around but if you look at the Balance Sheet under Liabilities there is $14.8 billion payable for the purchase of T-Bills and I also subtract the $4.8 billion from Railroad, Utilities and Energy since Insurance segment holds most of the cash.

That's my favorite Ben Franklin quote! LOL

Really interesting breakdown, thank you!